Why Your Mortgage Rate Isn't Set by the Bank: The Hidden Logic of the Bond Market

This fundamental misunderstanding of the capital markets often leads to misplaced expectations among borrowers and real estate professionals alike. The prevailing belief—that the Federal Reserve or local lending institutions unilaterally dictate mortgage rates in a closed boardroom—ignores the mechanical reality of the global financial system. To understand the true cost of homeownership, one must look past the bank teller and toward the volatility of the bond market, where mortgage pricing is determined by the real-time trading of Mortgage-Backed Securities (MBS).

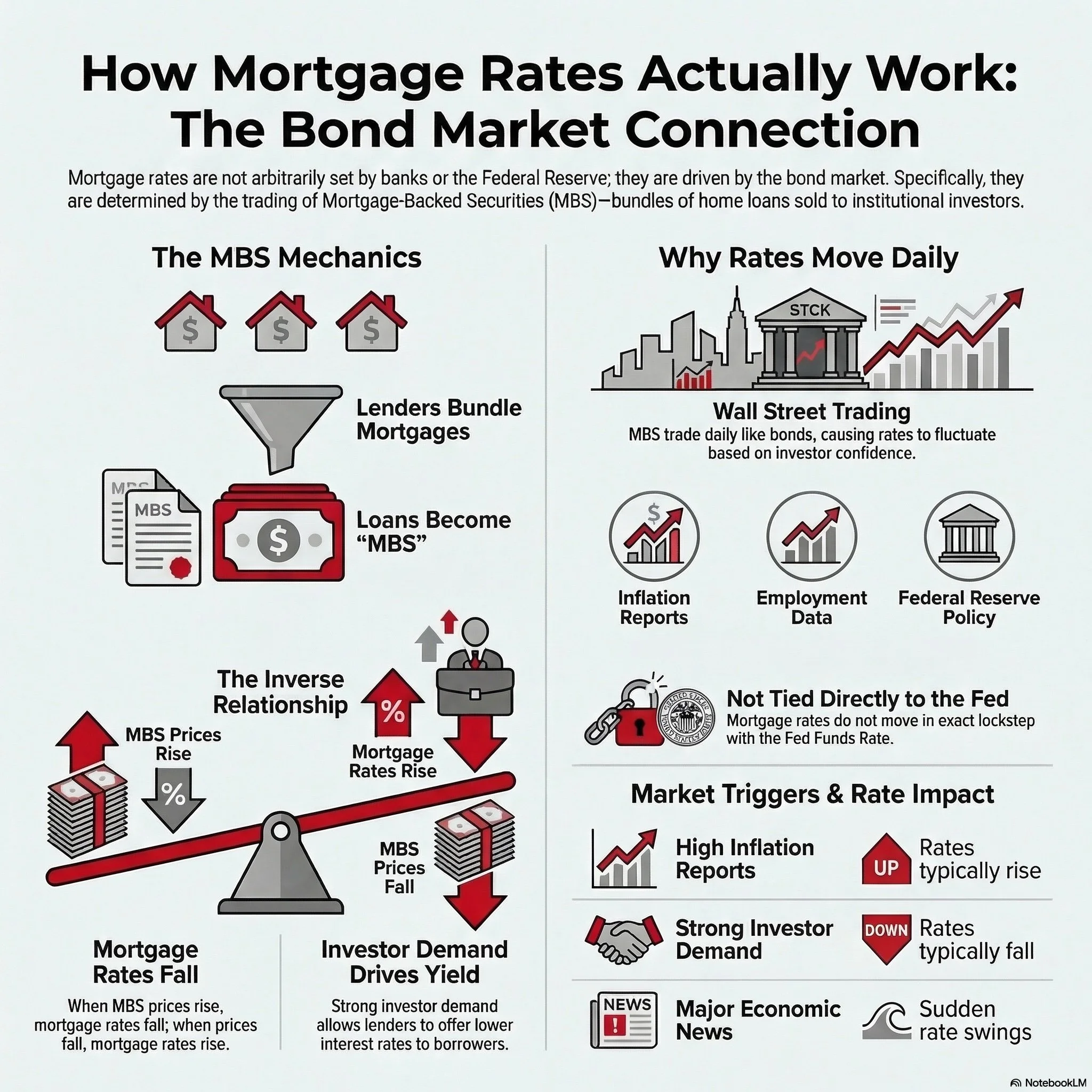

Your Loan is a Product, Not a Relationship

When a borrower executes a mortgage, the originating lender rarely retains that debt for the duration of its 30-year term. Instead, the modern mortgage is a financial commodity. Lenders package these individual loans into massive pools, which are then securitized and sold to institutional investors—including pension funds, insurance companies, and sovereign wealth funds—as Mortgage-Backed Securities.

This process of commoditization is the fundamental reason pricing is removed from the local bank level. Once a loan is bundled for the secondary market, the lender ceases to be a price-setter and instead becomes a price-taker. Because these loans must compete for capital against other global assets, their pricing is dictated by what global investors are willing to pay for the underlying stream of payments. Consequently, your local bank’s profit margin is secondary to the yield requirements of a pension fund manager halfway across the globe.

The Inverse Seesaw of Prices and Rates

The mechanics of mortgage pricing rely on a simple, inverse relationship between the price of the security and the interest rate (or yield) it offers. To navigate this market, one must grasp this core dynamic:

When MBS prices rise, mortgage rates fall.

When MBS prices fall, mortgage rates rise.

This relationship is governed by the shifting appetite of the investment community. As the market context dictates:

"Investors care about yield, which is their return. If investors are eager to buy mortgage-backed securities, they are willing to pay a higher price for them. When prices go up, the yield goes down. That allows lenders to offer lower mortgage interest rates."

If investor appetite wanes, prices must drop to entice buyers. To maintain a competitive yield at a lower purchase price, the interest rate charged to the borrower must increase. In this ecosystem, the borrower’s interest rate is effectively the "bribe" required to convince an investor to hold that debt.

Why Rates Have a "Daily Pulse"

Because Mortgage-Backed Securities trade with the same fluidity as equities or treasury bonds, mortgage rates possess a "daily pulse" that reacts to the shifting tides of the global economy. This volatility is not a matter of bank policy, but a reflection of market sentiment. Investors constantly recalibrate what they are willing to pay for MBS based on several key drivers:

Inflation reports

Federal Reserve policy shifts

Employment data

Global economic news

Investor demand for safer assets

This daily movement suggests that a borrower’s rate is effectively being "voted on" by the global market every minute the exchanges are open. Rather than a static figure, the mortgage rate is a living metric of investor confidence; when the outlook for the economy shifts, demand for these securities—and thus the rate available to a homebuyer—reacts instantly.

The Fed Funds Rate vs. Mortgage Reality

A frequent analytical error is the assumption that mortgage rates move in lockstep with the Federal Reserve’s "Fed Funds Rate." While the Fed influences the cost of short-term borrowing, mortgage rates operate on a different horizon. Mortgage-Backed Securities are long-term assets that react to forward-looking economic data and anticipated inflation, whereas the Fed Funds Rate is a specific, overnight rate for interbank lending.

Because MBS trade independently on Wall Street, they often move in anticipation of Fed news or even in the opposite direction if the market’s outlook differs from the central bank’s mandate. This independence means that mortgage rates often fluctuate based on news and demand cycles long before—or entirely independent of—an official announcement from the Federal Reserve.

The Big Picture for Borrowers and Agents

The mortgage market is a transparent reflection of the broader economy and the collective risk appetite of global investors. Pricing is not a localized decision but a result of the constant ebb and flow of supply and demand for Mortgage-Backed Securities. When inflation data or employment figures reach the wires, the bond market responds immediately, causing sudden swings that can impact a borrower's purchasing power in hours.

For real estate professionals and their clients, shifting focus from the local bank to the bond market provides a more accurate lens for timing a transaction. The strategic takeaway is clear: your interest rate is a global commodity traded on Wall Street every day. How does it change your perspective on market timing to know that your mortgage rate is being determined by the minute-to-minute sentiment of the world’s largest investors?